lower of cost or net realizable value, check these out | How do you calculate lower of cost or net realizable value?

The lower of cost or net realizable value concept means that inventory should be reported at the lower of its cost or the amount at which it can be sold. Net realizable value is the expected selling price of something in the ordinary course of business, less the costs of completion, selling, and transportation.

How do you calculate lower of cost or net realizable value?

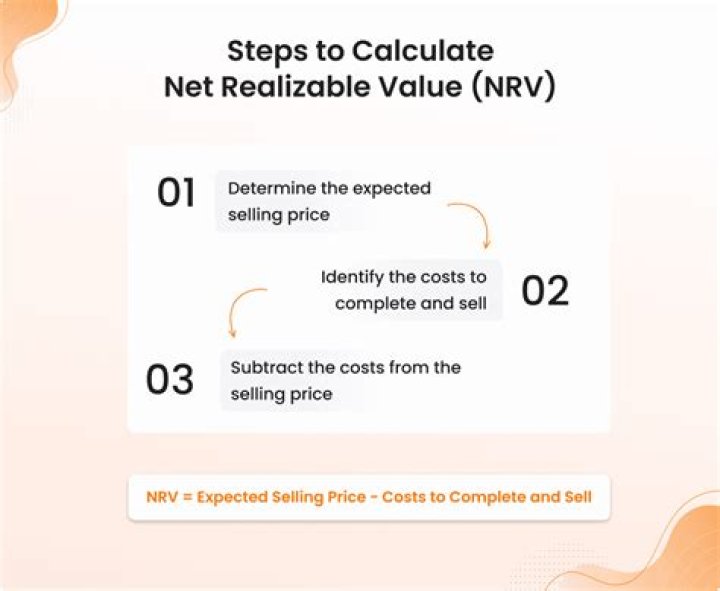

Determine the market value of the inventory item. Summarize all costs associated with completing and selling the asset, such as final production, testing, and prep costs. Subtract the selling costs from the market value to arrive at the net realizable value.

What is LC and NRV?

Generally accepted accounting principles require that inventory be valued at the lesser amount of its laid-down cost and the amount for which it can likely be sold—its net realizable value(NRV). This concept is known as the lower of cost and net realizable value, or LCNRV.

Is NRV always lower than cost?

Under normal circumstances, cost of inventory is always lesser than the net amount business can earn by selling the inventory, called net realizable value (NRV). Common sense dictates that cost has to be lesser than NRV to make profit.

How do you calculate net realizable value?

It is found by determining the expected selling price of an asset and all the costs associated with the eventual sale of the asset, and then calculating the difference between these two. To put it in formulaic terms, NRV = Expected selling price – Total production and selling costs.

When applying the lower of cost or net realizable value NRV means quizlet?

Net realizable value is defined as estimated selling price less purchase price.

What are the reasons for lower net realizable value?

Obsolescence, over supply, defects, major price declines, and similar problems can contribute to uncertainty about the “realization” (conversion to cash) for inventory items. Therefore, accountants evaluate inventory and employ lower of cost or net realizable value considerations.

Why are inventories valued at the lower of cost or net realizable value Lcnrv?

Why are inventories valued at the lower-of-cost-or-net realizable value (LCNRV)? Departure from cost is required; however, when the utility of the goods included in the inventory is less than their cost, this loss in utility should be recognized as a loss of the current period, the period in which it occurred.

Why is net realizable value important?

Computing for the Net Realizable Value is important for businesses to properly bring the valuation of their inventory and accounts receivable in order as to not overstate their assets. This is stated in the Generally Accepted Accounting Principles (GAAP) and International Financing Reporting Standards (IFRS).

When applying the lower of cost or net realizable value Lcnrv method inventory value reported Cannot exceed the?

Valuing Inventory at Lower of Cost or Market (LCM)

The replacement cost cannot exceed the net realizable value (NRV) The net realizable value.

When inventory cost is lower than NRV inventory should be reported at?

When the cost of the inventory is reduced to the NRV, the amount of the write down is reported as a loss on the income statement.

Is net realizable value the same as market value?

Net realisable value (NRV) is equal to selling price of the goods less the estimated cost of completion of the goods and the cost that would be incurred to sell the goods. Market value refers to the current or most recently-quoted price for a market-traded security.

What is the purpose of the lower of cost or market method?

The lower of cost or market method lets companies record losses by writing down the value of the affected inventory items.

When reporting inventory using the lower of cost or market method market should not be less than?

When reporting inventory using the lower of cost or market, market should not be less than: Net realizable value less a normal profit margin. The gross profit method can be used in all of the following situations except: In the preparation of annual financial statements.

Do write offs affect net accounts receivable?

Under the allowance method, a write‐off does not change the net realizable value of accounts receivable. It simply reduces accounts receivable and allowance for bad debts by equivalent amounts. Customers whose accounts have already been written off as uncollectible will sometimes pay their debts.

Which inventory method approximates inventory valuation at the lower-of-cost-or-market?

14. When the cost-to-retail ratio is computed after net markups (markups less markup cancellations) have been added, the retail inventory method approximates lower of cost or market. This is known as the conventional retail inventory method.

Which statement concerning lower-of-cost-or-market LCM is false?

Which statement concerning lower of cost or market (LCM) is incorrect? Under the LCM basis, market does not apply because assets are always recorded and maintained at cost.

When valuing raw materials inventory at lower-of-cost-or-market what is the meaning of the term?

When valuing raw materials inventory at lower-of-cost-or-market, what is the meaning of the term “market”? Replacement cost, Net realizable value, or Net realizable value less a normal profit margin. Prevents overstatement of the value of obsolete or damaged inventories.

Related Archive

harry potter wizards unite wand guide, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023

harry potter villain test, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023

harry potter uk edition books, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023