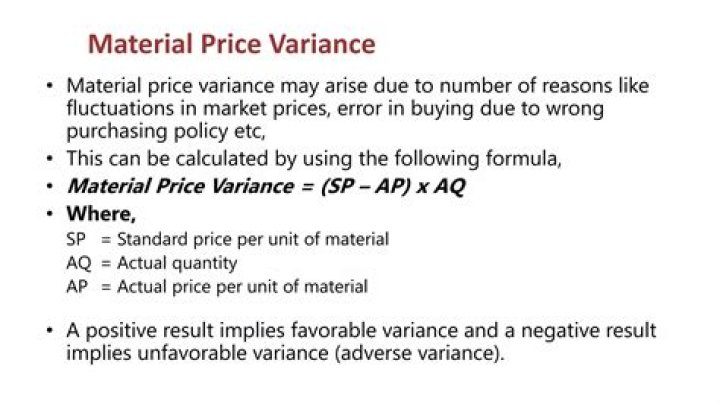

material price variance formula, check these out | How do you calculate material price variance?

Vmp = (Actual Quantity Purchased * Actual Unit Cost) – (Actual Quantity Purchased * Standard Unit Cost). When the Actual Materials Price is higher than the Standard Materials Price, the variance is said to be unfavorable, since the Actual price paid on materials purchased is greater than the allowed standard.

How do you calculate material price variance?

To calculate material price variance, subtract the actual price per unit of material from the budgeted price per unit of material and multiply by the actual quantity of direct material used.

What is the formula for material usage variance?

The formula for this variance is:(standard quantity of material allowed for production – actual quantity used) × standard price per unit of material. (standard quantity of material allowed for production – actual quantity used) × standard price per unit of material.

Why do you calculate material variance?

Material Cost Variance gives an idea of how much more or less cost has been incurred when compared with the standard cost. Thus, Variance Analysis is an important tool to keep a tab on the deviations from the standard set by a company.

What is the formula for calculating material price variance and material usage variance?

The actual cost of direct materials is : Actual quantity of direct materials x Actual price per unit of direct materials. usage or quantity variance, direct material cost variance can also be calculated as: Direct Material Cost Variance = Direct Material Price Variance Direct Material Usage or Quantity Variance.

What is the relationship between material price and material usage variance?

In variance analysis (accounting) direct material price variance is the difference between the standard cost and the actual cost for the actual quantity of material purchased. It is one of the two components (the other is direct material usage variance) of direct material total variance.

Who is responsible for material price variance?

Purchasing department is responsible to place orders for direct materials so this variance is generally considered the responsibility of purchase manager.

What is MCV in accounting?

Material Cost Variance (MCV) is the difference between the standard cost of the material allowed (standard material) for the output to be achieved and the actual cost of the material used. It is the aggregate of material price and usage variance.

How do you calculate labor and material variances?

The labor price variance is found by subtracting the actual paid rate from the standard budgeted rate and then multiplying it by the actual hours worked. The labor quantity variance is found by multiplying the standard rate by the difference of the standard hours budgeted minus the actual worked hours budgeted.

Related Archive

harry potter wizards unite wand guide, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023

harry potter villain test, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023

harry potter uk edition books, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023