property tax journal entry, check these out | How is property tax recorded in accounting?

How is property tax recorded in accounting?

Record Real Estate Taxes—Accrual Method of Accounting

Create a “Real Estate Tax Expense” account in the expense section of the general ledger. Create a “Real Estate Tax Payable” account in the liabilities section of the general ledger.

What is the journal entry for tax?

What Is the Journal Entry for Sales Tax? The journal entry for sales tax is a debit to the accounts receivable or cash account for the entire amount of the invoice or cash received, a credit to the sales account and a credit to the sales tax payable account for the amount of sales taxes billed.

Is property tax a prepaid expense?

Property taxes add another layer of complexity because they are a prepaid expense.

Is property tax expense an expense?

The IRS says you can deduct property taxes, but they put some limitations and restrictions on what portion of your property tax is deductible as a business expense: You can deduct the portion of your property tax that is levied based on the assessed value.

How do I enter property taxes in QuickBooks?

Click on Federal Taxes > Deductions & Credits. In the Your Home section, click on the Start/Revisit box next to Property Taxes. On the next screen, enter the property taxes in the box labeled Additional property (real estate) taxes.

Is tax an expense or liability?

Tax expense affects a company’s net earnings given that it is a liability that must be paid to a federal or state government. The expense reduces the amount of profits to be distributed to shareholders in the form of dividends.

How do you record provision for taxation?

Provision for Income Tax is simply calculated by multiplying the tax rate with the income before tax. This can be described using the formula below: Provision for Income Tax = Income Earned before Tax * Applicable Tax Rate.

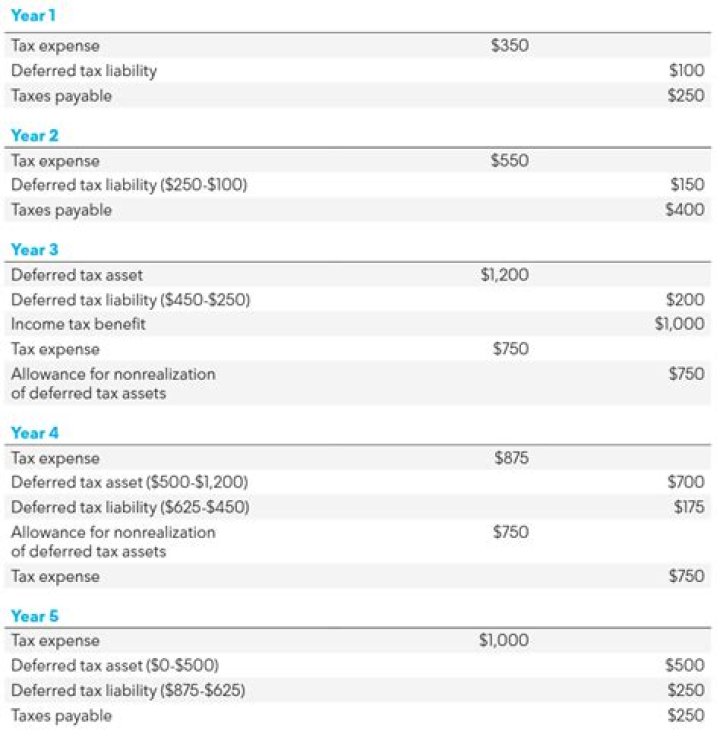

What is the journal entry for deferred tax asset?

For permanent difference it is not created as they are not going to be reversed. The book entries of deferred tax is very simple. We have to create Deferred Tax liability A/c or Deferred Tax Asset A/c by debiting or crediting Profit & Loss A/c respectively. The Deferred Tax is created at normal tax rate.

What is the 12 month rule for prepaid expenses?

The 12-Month Rule

The “12-month rule” allows for the deduction of a prepaid expense in the current year if the right or benefit paid for does not extend beyond the earlier of: 12 monthsfrom the date the prepayment is made, or. the end of the taxable year following the taxable year in which the payment is made.

What is the entry for prepaid expenses?

To recognize prepaid expenses that become actual expenses, use adjusting entries. As you use the prepaid item, decrease your Prepaid Expense account and increase your actual Expense account. To do this, debit your Expense account and credit your Prepaid Expense account. This creates a prepaid expense adjusting entry.

What is the difference between Prepaids and escrow?

Prepaid items are one-time charges, paid at the time a real estate transaction is closed, or finalized. Escrow accounts are a continuing expense, typically billed monthly by the lender.

Is property tax a business expense?

You can deduct property taxes you incurred for property used in your business. For example, you can deduct property taxes for the land and building where your business is situated. The property tax related to business use of workspace in your home has to be claimed as business-use-of-home expenses.

Where do property taxes go on the income statement?

This expense appears immediately before the calculation of net income occurs. Income taxes should not be confused with other “deductible” expenses such as property taxes, which is an overhead cost and should be included as an operating expense. Property taxes are sometimes categorized as Taxes Other than Income Taxes.

Can you deduct property taxes in 2020?

You can only deduct your property taxes in the year you pay them. If you’re filing your taxes for 2020, then, only deduct the amount of property taxes you paid in that year.

How do you record property purchases in accounting?

Add a home’s purchase price to the closing costs, such as commissions, to determine the home’s total cost. Write “Property” in the account column on the first line of a journal entry in your accounting journal. Write the total cost in the debit column. A debit increases the property account, which is an asset account.

Related Archive

harry potter wizards unite apple, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023

harry potter uniform shop, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023

harry potter wand name list, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023